Understanding Credit Scores: A Comprehensive Guide

Credit scores are vital for financial health, impacting loan approvals and interest rates. Learn how to manage and improve yours.

What is a Credit Score?

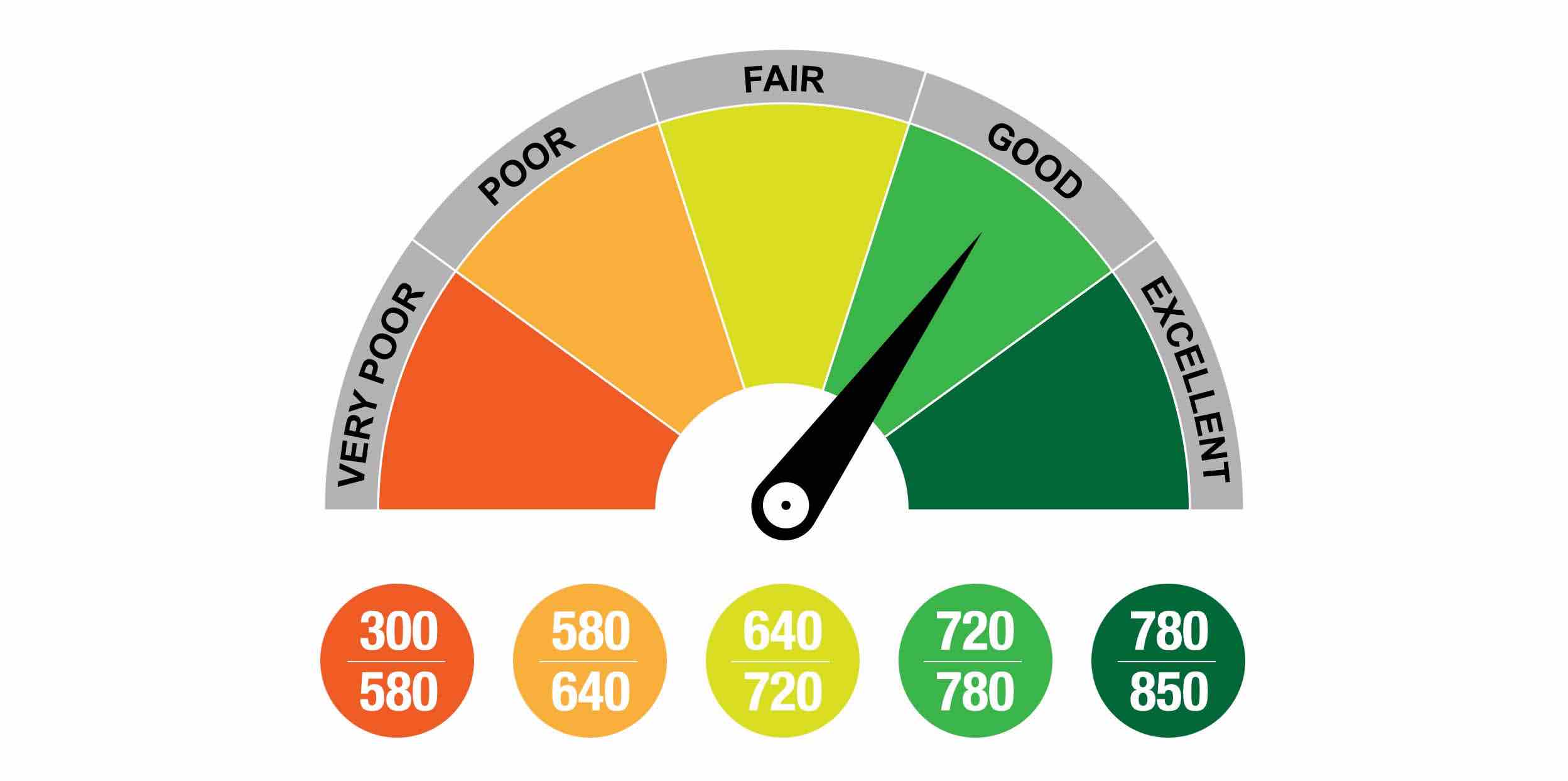

A credit score is a numerical representation of an individual's creditworthiness. Financial institutions, such as banks and credit card companies, use these scores to evaluate the risk of lending money or extending credit. Typically, credit scores range from 300 to 850, with higher scores indicating better creditworthiness. The score is calculated based on information from your credit report, which includes your payment history, outstanding debts, length of credit history, types of credit used, and recent inquiries into your credit report. Understanding your credit score is crucial because it affects your ability to obtain loans, secure favorable interest rates, and even impacts rental applications or job prospects. By maintaining a good credit score, you can save money on interest payments and gain access to better financial opportunities.

How Credit Scores are Calculated

Credit scores are calculated using complex algorithms that assess several factors. The most significant component is your payment history, which accounts for approximately 35% of your score. This aspect examines whether you pay your bills on time and in full. The amounts owed, or your credit utilization ratio, constitutes about 30% of your score. It measures how much of your available credit you are using. A lower ratio is preferable. The length of credit history contributes 15% and reflects the age of your oldest account, the age of your newest account, and the average age of all your accounts. The types of credit you use make up 10% of the score, rewarding a mix of installment loans and revolving credit. Lastly, new credit inquiries account for 10%, so opening several new accounts in a short period can lower your score.

The Importance of Credit Scores

Credit scores play a pivotal role in various financial aspects of life. They influence not only your ability to borrow money but also the terms and interest rates you will receive. A high credit score can save you thousands of dollars over the life of a loan by securing a lower interest rate. For instance, when applying for a mortgage, a strong credit score can mean the difference between an affordable monthly payment and financial strain. Furthermore, landlords often use credit scores to screen potential tenants, and employers might consider them during the hiring process. Insurers also use credit information to set premiums, which means a better score could lead to lower insurance costs. Thus, maintaining a good credit score is essential for financial health and achieving long-term financial goals.

Improving Your Credit Score

Improving your credit score requires a strategic approach and discipline. Begin by checking your credit report for errors, as inaccuracies can unfairly lower your score. You are entitled to one free report from each of the major credit bureaus annually. Once errors are corrected, focus on paying bills on time, as this is the most significant factor affecting your score. Reducing your credit card balances to lower your credit utilization ratio can also have a positive impact. Avoid opening several new accounts simultaneously, as each inquiry can slightly decrease your score. Instead, gradually build your credit history by responsibly managing existing accounts. Finally, consider becoming an authorized user on a responsible person's credit card account to benefit from their positive credit behavior.

Common Credit Score Myths

There are many misconceptions about credit scores that can lead to confusion. One common myth is that checking your own credit score will hurt it. In reality, checking your score is considered a soft inquiry and does not affect it. Another misconception is that closing old accounts will improve your score. However, closing accounts can reduce your available credit and increase your credit utilization ratio, potentially lowering your score. Many also believe that carrying a small balance on credit cards is beneficial, but paying off your balance in full each month is actually better for your score. Understanding these myths helps you make informed decisions about managing your credit effectively.

The Long-term Impact of Credit Scores

Your credit score has a lasting impact on your financial journey. A strong credit score can open doors to opportunities such as better loan terms, increased borrowing power, and financial flexibility. Conversely, a poor credit score can limit your options and cost you more in interest and fees. It's crucial to view credit management as a long-term commitment. Establishing good habits, such as making timely payments, maintaining low credit utilization, and monitoring your credit report, will serve you well over time. Remember, building and maintaining a good credit score is not just about immediate benefits but also about ensuring financial stability and success in the future. By prioritizing your credit health, you set the foundation for achieving your financial aspirations.